Glucagon-like peptide-1 receptor (GLP-1R) therapeutics are not the only contributors to the rapidly growing global obesity market. The non-GLP-1R landscape, including calcitonin receptor (CR) products, is emerging, with sales expected to surge 50-fold over the next five years.

Obesity is a chronic condition, characterised by excessive fat, which increases the risk of serious diseases such as type 2 diabetes. In the US, the obesity rate has steadily increased, with the condition affecting over 100 million adults, 40%–42% of the adult population. Accordingly, the pharmaceutical market for obesity drugs is growing at an unprecedented rate. In 2031, GlobalData’s sales and forecast tool predicts obesity drugs to collectively generate $172.6bn, a rise of 139% from the $72.2bn forecast for 2026. This growth has largely been driven by the commercial successes of GLP-1R agonists, such as Novo Nordisk’s semaglutide (Wegovy) and Eli Lilly’s tirzepatide (Zepbound).

Go deeper with GlobalData

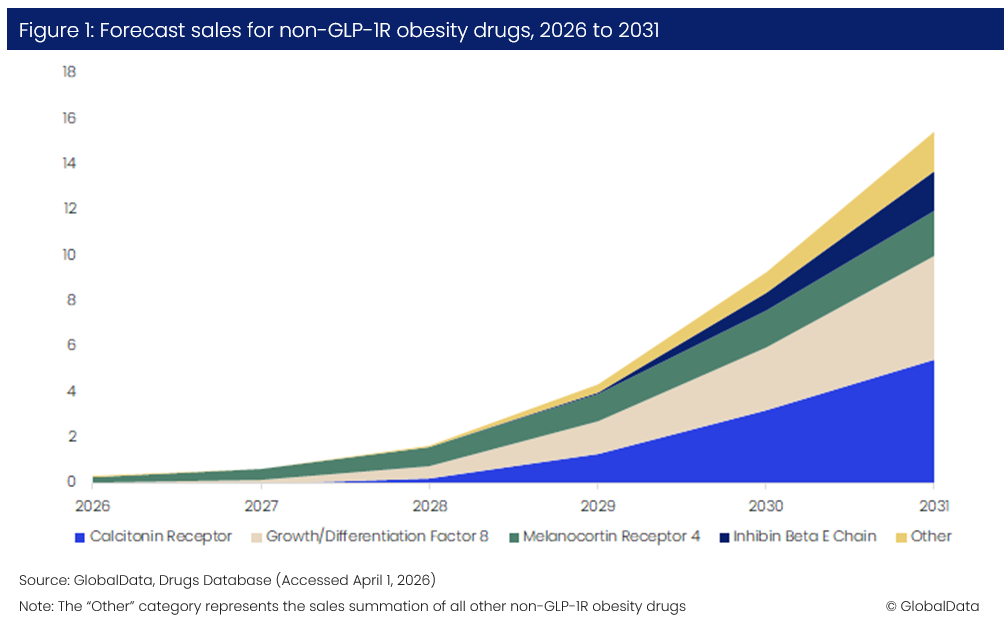

Despite their current dominance, GLP-1R agonists are not the only contributors to future growth. Currently, there is limited interest in the non-GLP-1R obesity field, as sales for obesity drugs targeting alternative mechanisms are only forecast to generate a mere $310m in 2026. However, by 2031, this figure is expected to surge almost 50-fold, indicating a strong market potential outside of GLP-1R drugs (Figure 1).

Due to a limited number of commercialised products, growth for the non-GLP-1R obesity landscape is forecast to remain low for the first two years (2026–2028), with $1.7bn estimated to be generated in 2028. From here, the market is expected to grow rapidly at a compound annual growth rate of 110.8%, ultimately reaching $15.5bn globally in 2031. The first launches for the obesity drugs targeting CR and inhibin beta E chain are estimated for 2028, facilitating the growth expected from this year.

By 2031, CR drugs are forecast to be the top non-GLP-1R obesity drug type, generating $5.43bn, equivalent to 35% of all sales attributed to non-GLP-1R drugs. The obesity heavyweights, Eli Lilly and Novo Nordisk, are expected to extend their dominance beyond GLP-1Rs, as they account for the top two CR drugs. By 2031, Eli Lilly’s eloralintide is forecast to lead the pack, generating $3.4bn, followed by the $771m attributed to Novo Nordisk’s cagrilintide. This expansion by the two largest obesity players into CR drugs suggests both companies are actively diversifying beyond GLP-1R drugs to secure early positions in emerging segments of obesity.

Elsewhere, the melanocortin receptor 4 represents the third largest non-GLP-1R obesity market. In 2031, this landscape is forecast to generate $2bn, a growth of over seven times the value for 2026. Sales for this category are solely attributed to one drug, Rhythm Pharmaceuticals’ setmelanotide (Imcivree), highlighting the limited competition within this space.

The obesity market is beginning to diversify, with non-GLP-1R drugs demonstrating strong long-term market potential as new mechanisms move closer to commercialisation. The key launches anticipated for 2028 are expected to facilitate the shift of this market from slow early growth to rapid expansion, reflecting confidence in alternative targets such as the CR. GLP-1R therapies are expected to remain the dominant force within obesity. However, companies are strategically investing in novel mechanisms to reduce reliance on this single drug class, securing positions within emerging segments. This diversification is likely to drive competition, expand treatment options, and reshape the long-term structure of the obesity pharmaceutical landscape.