Japan’s latest National Health Insurance (NHI) drug price revision for FY26 has now come into effect, with an average 4.02% reduction in drug prices on a spending basis across roughly 15,800 products. While this is slightly lower than the 4.67% reduction recorded in FY24, this year’s revision includes multiple overlapping mechanisms such as the expansion of G1 repricing, adjustments to the Patent-Period Price Maintenance Program (PMP), and broader inclusion of biologics in the price reduction mechanisms. The analysis below therefore, reviews the FY26 price revision by comparing the recent NHI-related price adjustments with observed price changes for the overall Japanese market in April 2026.

NHI drug price revisions for FY26 account for 61% of the products receiving price reductions

Based on findings from GlobalData’s Price Intelligence (POLI), 73% of products recorded a price change in April 2026. While 27% of products saw no price change, 61% of drugs received price cuts and 12% of drugs price increases. Of those medicines that had a price change in April 2026, most (83%) experienced price reductions in April, reflecting an overall negative trend in the price revisions, with price cuts outweighing the price increases across the market.

Go deeper with GlobalData

Japan performs scheduled biennial price adjustments as a cost-reduction method, where these adjustments are applied through specific mechanisms, such as the market price-based repricing and expanded G1 eligibility. In the FY26 price revision, the number of products qualifying for the G1 repricing has also significantly increased due to the expanded eligibility requirement. Under the revised framework, all long-listed, off-patent products (LLPs) that pass the replacement period will be subjected to the G1 rule, regardless of their generic substitution rate. Additionally, biologic originators will also be subjected to the G1 rule if their biosimilars are listed on the NHI. As such, LLPs face a greater risk of receiving substantial price reductions for five years following the first NHI-listed generic.

Despite the downward pricing pressure, price increases were also applied to certain products as part of the FY26 price revisions, demonstrating that upward adjustments are still being used to support unprofitable, supply-sensitive drugs in order to maintain a stable supply alongside cost-containment efforts.

Expanded scope of G1 repricing rules

As mentioned, one of the main changes for the FY26 revision is the expansion of the G1 repricing framework, which now captures a broader set of off-patent drugs and includes biologics with biosimilar competition. Under the updated rules, eligibility is no longer tied to substitution thresholds, but instead reflects whether the drug has been exposed to competition over time. As a result, the widened scope of repricing has increased the number of products subjected to price reductions.

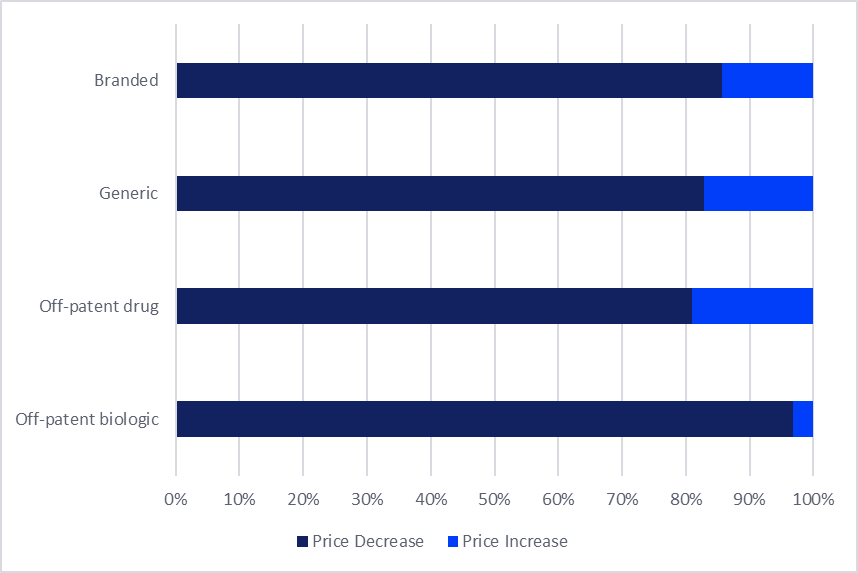

Overall, it appears that pricing pressure under the FY26 revision is most concentrated among off-patent products, particularly those exposed to sustained competition. Among the off-patent biologics, 95% experienced price reductions last month. Furthermore, approximately 69% of off-patent (originator) small molecules recorded a price decrease, indicating that a majority of the products in this category have been affected by the downwards price adjustments. In comparison, during the last biennial price revision in 2024, 57% of all off-patent small molecules saw price reductions. In addition to the FY26 price revisions affecting a larger share of products, the latest price revisions also include more significant price cuts. For example, Roche’s (Switzerland) anti-cancer biologic Avastin (bevacizumab) under the FY26 revision received an average price cut of 45%.

Figure 2: Percentage of products that received price increases versus reductions in Japan per drug type in April 2026

Price protection continues, alongside deferred price reductions

In FY26, the Price Maintenance Premium (PMP) scheme has been renamed the Patent-Period Price Maintenance Program for Innovative Drugs. The PMP continues to support pricing for innovative, branded drugs, allowing certain products to maintain their NHI-listed prices during the patent-protected period. The FY26 revision also expands certain premium mechanisms, including the ability to receive both marketability and pediatric premiums. However, PMP is not absolute. As outlined in the reform, drugs with larger gaps between the NHI-listed price and actual market price may still be subjected to downward adjustment.

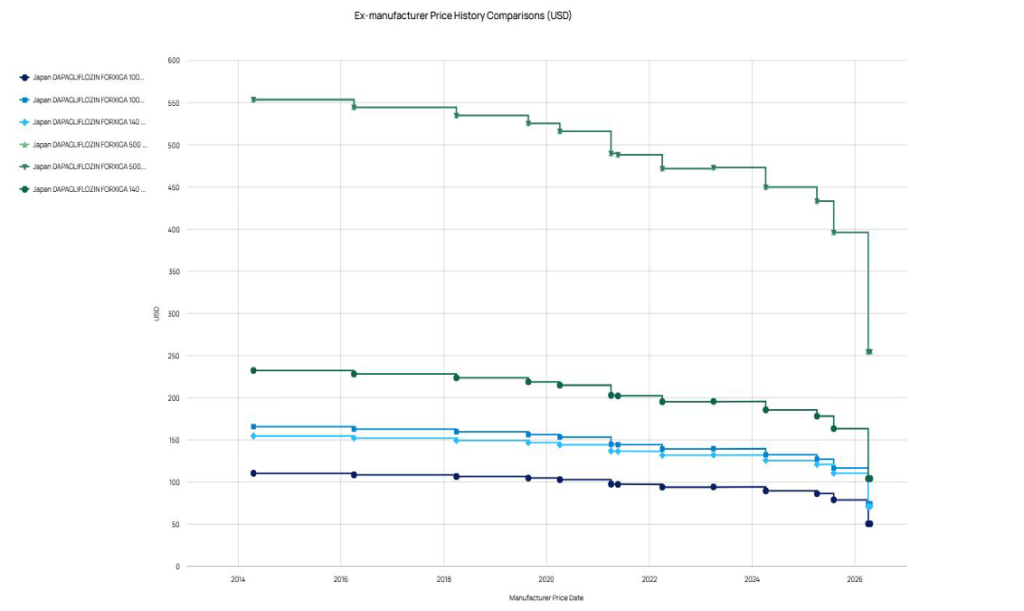

Deferred PMP repricing is also more visible, where adjustments apply to products that avoided earlier price reductions during their protection period and are now subjected to price cuts. Several widely used therapies have been affected, with some reductions exceeding 20%, and in a few cases, reaching above 30%. Examples include AstraZeneca’s (UK) Forxiga (dapagliflozin), shown in Figure 3 below, receiving the largest price reduction rate, an average of 36% across all packs, followed by Taiho Pharmaceutical’s (Japan) Abraxane (paclitaxel), which saw price reductions exceeding 30%.

Figure 3: Manufacturer price history (EUR) of Forxiga in Japan

Compared to the previous round of biennial price revision, the FY26 reform had a smaller NHI price reduction average rate of 4.02% on a drug spending basis. However, the revision expanded the G1 repricing framework to include more LLPs and biologics with competition, increasing the number of products subject to price cuts. The majority of the products in April 2026 experienced reductions in Japan, largely targeting off-patent originator medicines. Simultaneously, the PMP scheme under its new name continued to protect some branded (patent-protected) drugs, while certain branded medicines received deferred price reductions when the market price gap was significant and therefore contributed to the total number of products that underwent price cuts in April.

This article is produced as part of GlobalData’s Price Intelligence (POLI) service, the world’s leading resource for global pharmaceutical pricing, HTA and market access intelligence integrated with the broader epidemiology, disease, clinical trials and manufacturing expertise of GlobalData’s Pharmaceutical Intelligence Center. Our unparalleled team of in-house experts monitors P&R policy developments, outcomes and data analytics around the world every day to give our clients the edge by providing critical early warning signals and insights. For a demo or further information, please contact us here.