Blockades by both Iran and the US in the Strait of Hormuz, as they negotiate an end to the conflict, continue to drive up healthcare costs globally. The shock to global trade risks triggering a sustained period of higher medical inflation, while cost-of-living crises threaten healthcare affordability and consumer spending on health in H2 2026.

Rising medical costs, which are caused in part by the external trade pressure in the Gulf, are a key risk factor driving household debt and widening access inequality globally. Weaker economies may have a reduced capacity for public healthcare spending growth. Healthcare systems, especially in low- and middle-income countries (LMICs), may also struggle to absorb mounting costs while maintaining service quality. Meanwhile, the financial strain on households from rising out-of-pocket healthcare costs could result in a shift toward lower-cost treatments or decisions to defer treatment. Poorer patient outcomes would have negative long-term consequences for public health systems, which will have to deal with more severe and difficult-to-treat cases. Given the elevated geopolitical uncertainty, serious shortages of medical products in some countries can no longer be discounted. Certain products becoming more difficult to obtain in the coming months could exacerbate price increases.

Go deeper with GlobalData

The possibility of prolonged disruption to trade in the Strait of Hormuz risks exacerbating the existing supply bottlenecks and inflation-driven cost challenges. As government authorities across the globe begin to publish inflation data for the period of trade disruption caused in the wake of the Strait of Hormuz blockades, the scale of the inflation shock for the healthcare sector should slowly become more visible.

The impact of higher medical cost inflation is not evenly spread. The problem is generally more manageable in advanced economies. That said, anxiety about medical supplies has led South Korean authorities to warn against price collusion, while Japan’s Prime Minister Sanae Takaichi released part of the country’s pandemic stockpile after the hospital sector came under financial pressure caused by the impact of low pricing, inflation, and a weaker national currency, which combined to increase costs for the import-dependent healthcare system.

Nevertheless, LMICs with a high reliance on medical imports are more exposed to spikes in healthcare cost inflation. In May 2026, the UN Department of Economic and Social Affairs forecast that inflation in developing countries will accelerate from an average of 4.2% to 5.2% in 2026, as higher import costs, higher costs for energy, and higher costs for transportation erode incomes and consumer spending power. The risk of “second round” medical inflation effects is also pronounced in energy-importing emerging economies such as the Philippines and Turkiye, especially as these countries are also combatting national currency depreciations. GlobalData has identified several examples of other emerging economies that are exposed to potential double-digit spikes in medical cost inflation over the next three years, including Indonesia, Singapore, South Korea, Taiwan, Thailand, and Vietnam. While the introduction of new medical technologies and therapeutic advances will account for a large proportion of upward trends in medical inflation in some of these markets, supply chain disruptions and protectionist trade policies also account for a significant share.

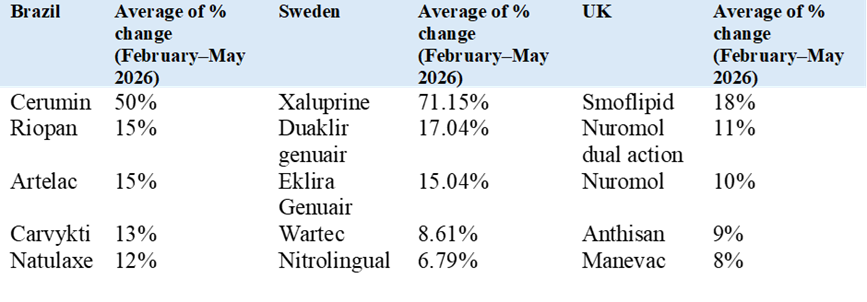

According to GlobalData’s POLI, the ongoing supply crisis is contributing to price increases. Looking at the pharmaceutical sector directly, research by GlobalData’s POLI reveals significant price increases for certain prescription medicines. While some medicines were already subject to price increases associated with other factors (i.e., shortages, the blockades in the Strait of Hormuz are exacerbating underlying trends). To quantify the impact of these price increases, the table below summarises the top five drugs with the greatest price increase in selected markets (Brazil, Sweden, and the UK) by comparing prices in February 2026 versus May 2026.

Figure 1: Average price change (%) for the top five drugs with the greatest price increase, February–May 2026 (Brazil, Sweden, and UK)

As the US-Israel war with Iran continues, manufacturing and transport costs may continue to surge, driven by higher fuel, shipping, and aviation freight costs. Pressure on manufacturers will likely intensify, worsening shortages of some products and medicine withdrawals from certain markets, and ultimately accelerating price increases. While some advanced markets may consider that tightening supplies is driving up medicine prices, other markets may increase stockpiling. This would likely be a contributing factor to larger inflationary pressure as countries compete for scarce supplies.

This article is produced as part of GlobalData’s Price Intelligence (POLI) service, the world’s leading resource for global pharmaceutical pricing, HTA and market access intelligence integrated with the broader epidemiology, disease, clinical trials and manufacturing expertise of GlobalData’s Pharmaceutical Intelligence Center. Our unparalleled team of in-house experts monitors P&R policy developments, outcomes and data analytics around the world every day to give our clients the edge by providing critical early warning signals and insights. For a demo or further information, please contact us here.