On 12 May 2025, US President Donald Trump signed an executive order directing the US Department of Health and Human Services (HHS) to secure Most Favored Nation (MFN) pricing for medicines. Central to this policy is the introduction of International Reference Pricing (IRP), a mechanism that benchmarks US drug prices against those in selected comparator markets. The framework consists of three IRP models: GENEROUS (GENErating cost Reductions fOr US Medicaid), GLOBE (Global Benchmark for Efficient Drug Pricing) and GUARD (Guarding US Medicare Against Rising Drug Costs), each incorporating a basket of international reference countries, many of which are European markets.

Given the US’s massive influence on global pricing, the inclusion of European markets in these IRP baskets introduces potential spillover effects impacting a product’s launch, pricing strategy, market prioritisation, and possible withdrawals in European countries. To explore whether these dynamics are already influencing industry behaviour, GlobalData analysed the product launch and withdrawal trends using its Price Intelligence (POLI) database, comparing activity in the ten months before (12 July 2024 – 12 May 2025) and after (12 May 2025 – 12 March 2026) the policy’s announcement.

Go deeper with GlobalData

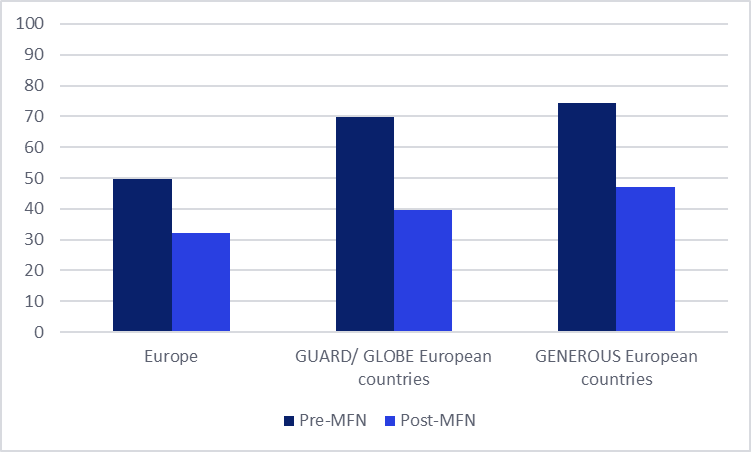

Impact of MFN pricing on European pharmaceutical launch activity

GlobalData’s Price Intelligence (POLI) analysis indicates a noticeable drop in the number of pharmaceutical launches across Europe, with an overall decline of 35% in the ten months following the introduction of IRP in the US compared to the previous ten months. A similar trend (37%) is observed when focusing on the countries included in the US reference baskets, specifically in the GENEROUS model (Denmark, France, Germany, Italy, Switzerland, and the UK). The GLOBE and GUARD models reference a broader set of European countries (14 of the 17 countries referenced in total), including Austria, Belgium, the Czech Republic, Denmark, France, Germany, Ireland, Italy, the Netherlands, Norway, Spain, Sweden, Switzerland, and the UK. Of the European markets referenced in the GLOBE and GUARD model, the average number of launches in these markets has declined by 43% in the ten months following MFN compared to the ten months prior.

It is important to acknowledge that while other factors could have contributed to this drop (such as regulatory delays, pricing and reimbursement negotiations, or supply chain constraints), the trend could be seen as an early signal of the impact that the introduction of IRP in the US may have on European markets. Based on the MFN policy framework and reference baskets, the lowest-priced markets are used as a reference point for US pricing. Consequentially, there is a structural disincentive to launch early in countries where prices are significantly lower, and pharmaceutical companies may be deliberately delaying the launch of their products in certain European markets. Additionally, US biotech firms have reportedly become wary of entering into licensing agreements with European partners in case they might be accused of inadvertently triggering MFN provisions that could erode US pricing. Heightened uncertainty may therefore be responsible for the strategic delay observed across Europe.

Figure 1: Average number of innovative medicines launches within Europe during the ten months before and after the MFN executive order announcement

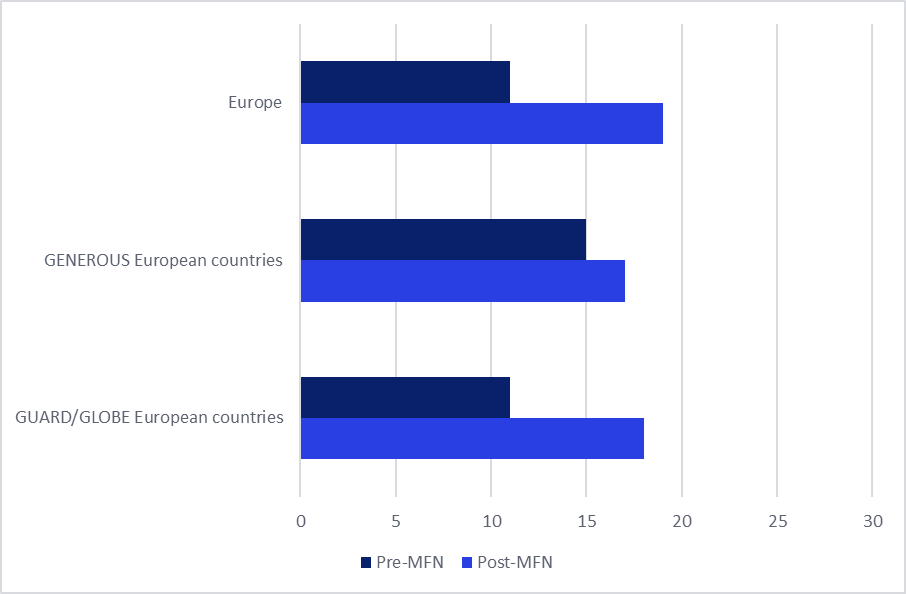

Greater product withdrawals across Europe after MFN introduction in the US

Parallel with reduced launch activity, withdrawal rates for branded medicines have increased sharply. According to GlobalData’s Price Intelligence (POLI) data, across Europe, the number of brands for which at least one pack has been withdrawn from the market has increased by 43% in the ten months following the MFN executive order. A similar trend is observed in the specific European markets referenced under the GENEROUS, GLOBE, and GUARD models. However, the increase is less pronounced in the core European countries included in the GENEROUS basket (10% increase) compared to European countries listed in the basket for the GLOBE and GUARD models (40%).

While this pattern is consistent with the expected effects of MFN pricing, it is important to note that product withdrawals can be driven by other factors, such as manufacturing constraints or failed site inspections, for instance. As such, the observed increase cannot fully be attributed to MFN-related pricing pressures alone. That said, MFN-related pricing pressure could be one of the several factors contributing to the higher withdrawal rates, as manufacturers could be faced with a difficult situation; either maintain access in lower-priced European markets where financial viability is now questioned or protect pricing integrity in the US. The observed increase in withdrawal rates from the data suggests that in some cases, companies could be opting for the latter. An example of this is Amgen’s Repatha, which was recently withdrawn from Denmark’s pharmaceutical market, one of the countries included in all three MFN models. It is likely linked to the low tender price available in Denmark, which can conflict with the companies’ efforts to maintain higher prices outside the US under MFN rules. This removal may be the start of a growing problem, where more pharmaceutical companies that are unable to obtain higher European prices may ultimately choose to withdraw their products rather than jeopardise their US market prices under the MFN IRP system.

Simultaneously, the policy environment in Europe could also add another layer of complexity. Governments are increasingly focusing on controlling pharmaceutical spending. For example, Italy has recently taken steps to curb rising medical expenditure and has hinted at resistance to higher European drug prices linked to MFN expectations. This growing disconnect between pricing pressure and national cost-containment policies may drive further medicine withdrawals across Europe.

Figure 2: Average number of brand withdrawals in Europe, before and after MFN introduction

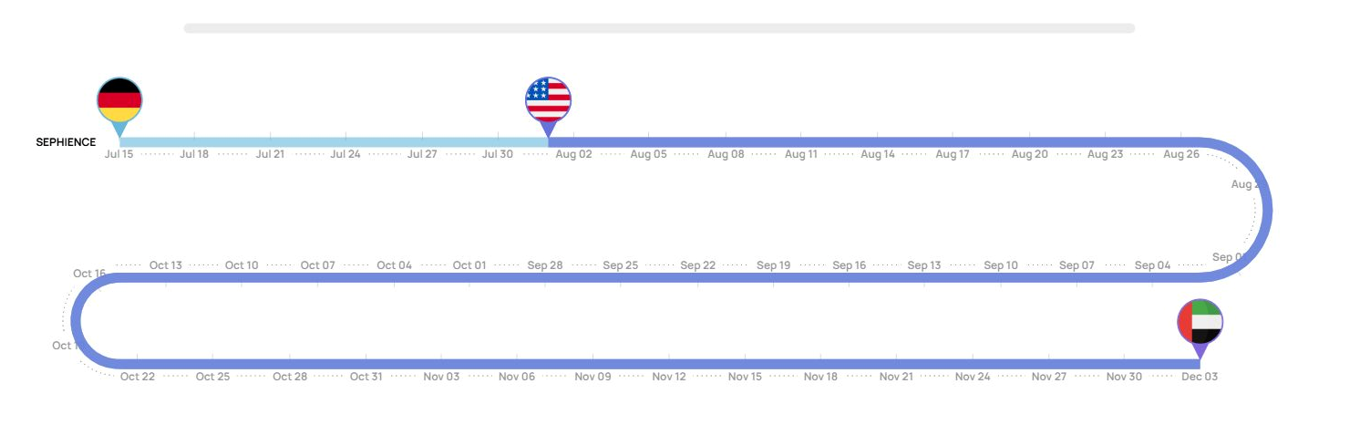

Early MFN impact on launch sequence

While it may be too early to draw conclusions on the impact of MFN on product launch sequence, early observations from products approved in 2025 continue to reflect a US-first launch pattern. Approximately 92% of these products were initially launched in the US, and of these, 97% have yet to be introduced in other markets. Among the smaller group of products that were launched outside the US, primarily Europe, 60% were first launched in Germany. Notably, all of these products have subsequently expanded into additional markets, with the US consistently included as one of them. An example of this is PTC Therapeutics’ Sepiapterin (Sephience), which was first launched in Germany after the MFN announcement, followed by the US and the United Arab Emirates (UAE). Overall, these early launch trends suggest continuity rather than disruption to the global launch pattern. While the limited and slower expansion into other markets may suggest increasing caution among pharma companies, it cannot yet be directly attributed to MFN.

Figure 3: Launch Sequence of Sepiapterin (Sephience)

While MFN pricing was initially proposed to address the high prices of medicines in the US, early trends suggest potential wider international effects, particularly for Europe. Fewer medicine launches and rising withdrawal rates in European markets may indicate that a growing number of companies are adjusting their strategies to protect US prices. This could mean increased delays in access to new therapies and more withdrawals of products from lower-priced European markets. Early trends from the 2025 launch sequence confirm the continued US-first strategy, with most yet to reach other markets. The potentially slower expansion, combined with the increased withdrawal rates, could suggest increased caution among pharmaceutical companies under MFN pricing pressures, although it’s too early to draw firm conclusions. While the policy may succeed in reducing drug prices in the US, it raises an important question about its broader impact on patient access and affordability across the pharmaceutical landscape. Additionally, if withdrawal rates and supply constraints intensify, policymakers will likely face pressure to make price adjustments to ensure continued access to medicines.

This article is produced as part of GlobalData’s Price Intelligence (POLI) service, the world’s leading resource for global pharmaceutical pricing, HTA and market access intelligence integrated with the broader epidemiology, disease, clinical trials and manufacturing expertise of GlobalData’s Pharmaceutical Intelligence Center. Our unparalleled team of in-house experts monitors P&R policy developments, outcomes and data analytics around the world every day to give our clients the edge by providing critical early warning signals and insights. For a demo or further information, please contact us here.