The biotech industry is currently in a bear market, creating both potential opportunities and pitfalls for CMOs. If bio/pharmaceutical companies fail, they will renege on their contract manufacturing agreements, but larger CMOs could also benefit by acquiring manufacturing sites from bankrupt companies, especially at a time when there is appetite for situating pharma production in the US.

A bear market is when a market experiences prolonged price declines. Typically, securities prices fall 20% or more from recent highs amid widespread pessimism and negative investor sentiment. The bear market for biotech companies started in 2021. At the time of writing in H1 2022, there are more than 100 public biotechs with negative enterprise values (when debt and/or cash exceeds the market capitalisation of a company), and no marketed drugs to generate from which to generate revenues. Pipeline-only portfolios mean that these companies cannot depend on drug sales to fund operations if investment should dry up in future. This level of contraction of the biotech market is significant and will particularly impact small CMOs, since they rely on smaller biotechs, many of which are now struggling, and may not be able to pay CMOs or sign new contracts.

Go deeper with GlobalData

The Nasdaq Biotechnology Index and the S&P Biotech ETF, which indicate public biotech performances, fell by 15 to 20% between 1 January and 18 March 2022. There were fewer IPOs in 2022 than 2021 in the biopharma industry, and also more widely in the market.

A company has a negative enterprise value if it has more cash on its balance sheet than its market value and debt. Biotech company shares have fallen in the last four months. It is possible that the ‘funding window’ has closed and investors are no longer interested in the company. The company might have trouble raising future cash.

Negative enterprise values do not have to spell disaster for biotechs, as a decline in biotech valuations may spark M&A in the sector and renewed support for product development from acquirers. Although the biotech sector is currently suffering, there are enough long-term buyers, including well-funded venture capitalists that see biotech as a megatrend, to keep capital flowing into the sector.

The CMO industry could benefit from the current predicament if they buy manufacturing assets from struggling public biotechs. This would allow CMOs to boost their production capacity and enhance capabilities at reasonable prices.

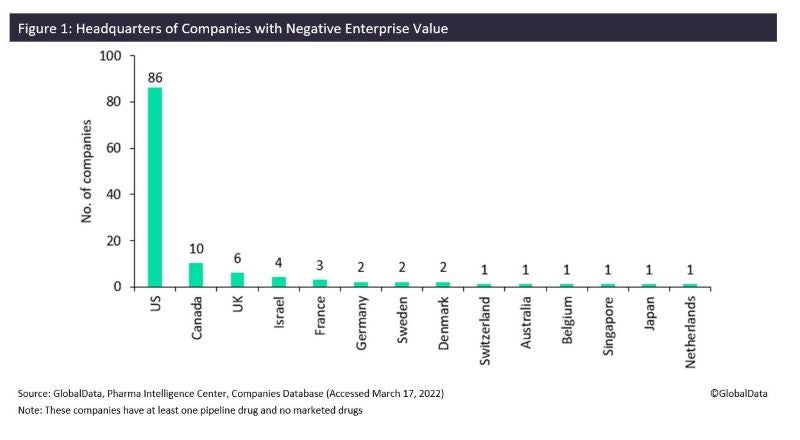

As Figure 1 shows, most pipeline bio/pharmaceutical companies with negative enterprise values are headquartered in the US. Most pipeline companies do not possess manufacturing facilities, but any they do own are likely to be in the US, as small companies tend to own sites local to their headquarters. US pharma facilities are highly sought after by CMOs as they are based in the largest pharmaceutical market globally. In recent years the US and Europe are increasingly discussing ‘onshoring’ pharmaceutical manufacturing, given Covid-19-related supply chain disruption, and CMOs can use this opportunity to acquire US sites to improve supply chain security.

Negative enterprise value companies may not fulfil contracts

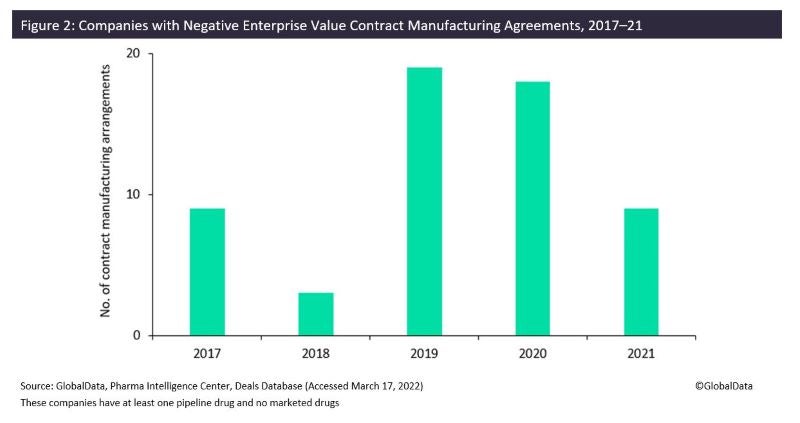

All companies in Figures 1 and 2 have a market cap below $1 billion. Small cap companies (with a market cap of less than $2 billion) tend to use CMOs as a necessity as they lack the internal manufacturing capabilities to produce their drugs. As Figure 2 shows, pharma companies with negative enterprise values have signed at least 94 contract manufacturing agreements since 2017, with both large and small CMOs alike. This is a substantial number of deals, although with an associated small scale of manufacturing due to their drugs being in clinical stage. The figure shows a tendency to increase the number of contract manufacturing agreements over time, as these are young companies with few pipeline products, outsourcing more manufacturing agreements as their lead product matures. If some of these bio/pharmaceutical companies fold, they will not be able to pay CMOs for the services they have contracted. All companies in Figures 1 and 2 have a market cap below $1 billion. Small cap companies (market cap less than $2 billion) tend to use CMOs as a necessity as they lack the internal manufacturing capabilities to produce their drugs.