Eliquis (apixaban) is one of the most commercially consequential loss-of-exclusivity (LOE) events in recent pharmaceutical history, with patent expiries expected this year for Europe and in 2027 for the US and Japan. With global sales of $14.4bn in 2025, the Bristol Myers Squibb (BMS) and Pfizer-partnered anticoagulant ranks among the industry’s highest-grossing small molecules. Its long-standing clinical adoption and expansive prescriber base have made it the dominant oral anticoagulant globally, but also a brand whose exclusivity loss carries outsized revenue implications for BMS.

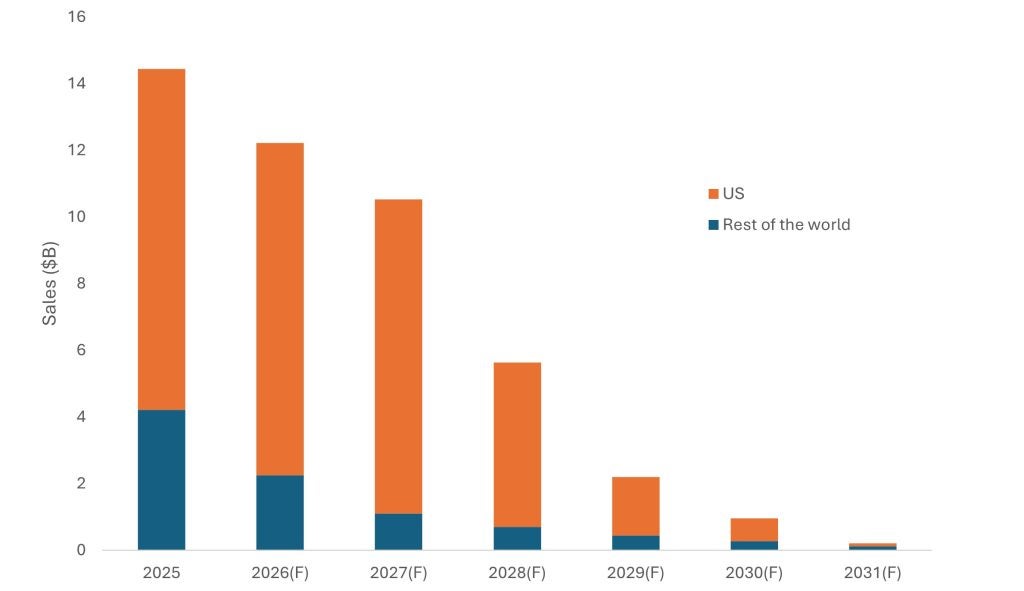

First approved in the EU in May 2011 and by the FDA in December 2012, Eliquis is a small molecule direct factor Xa inhibitor indicated across stroke prevention, atrial fibrillation, and venous thromboembolic conditions, including deep vein thrombosis and pulmonary embolism. As illustrated in Figure 1, global Eliquis sales are forecast to fall from $14.4bn in 2025 to $205m in 2031, a near-total erosion of 98.6% and one of the largest single-asset LOE events in the industry. The decline is not gradual but geographically sequenced: European exclusivity loss in May 2026 triggers the first wave of compression, followed by the far larger US cliff in 2028, which drives the steepest absolute revenue destruction. In total, the brand is projected to shed $14.2bn over six years.

Go deeper with GlobalData

Eliquis global sales forecast by geography, 2025-2031

The first phase of erosion is concentrated in ex-US markets. Rest of World revenues are forecast to fall by nearly 75% between 2025 and 2027 as European generic entry takes hold, driven by tendering systems and formulary-level switching that can displace branded volume rapidly once exclusivity lapses. The US, by contrast, is expected to remain largely insulated through this period, its share of total portfolio revenues rising to nearly 90% by 2027 as the brand becomes increasingly concentrated in its last high-value geography.

US revenue erosion is expected to begin before generic entry. Under the Inflation Reduction Act, a Medicare maximum fair price of $231 per 30-day supply took effect in January 2026, reducing net revenues two years ahead of the patent cliff. When US exclusivity falls in 2028, the impact is projected to be immediate and severe—a near-50% single-year decline driven by the rapid generic substitution dynamics of the US market, where formulary switches and substitution-at-dispensing can shift volume within quarters of launch. By 2031, US revenues are forecast to have fallen 99% from their peak in 2025, accounting for over $10bn of total losses across the forecast period.

The key competitive intelligence signal is not the LOE date itself—long anticipated by the market—but the speed and scale of post-exclusivity revenue compression that follows generic entry across sequential geographies. The Eliquis cliff is reshaping BMS’s capital allocation strategy, with multibillion-dollar acquisitions of Karuna Therapeutics ($1bn) and RayzeBio ($4.1bn) representing deliberate bets on neuroscience and radiopharmaceuticals as replacement growth platforms. The Karuna acquisition has already delivered a launched asset: Cobenfy (formerly KarXT) received FDA approval in September 2024 as the first new class of schizophrenia treatment in over 50 years, and launched commercially in the US in late 2024—signalling that BMS’s M&A-led repositioning is beginning to bear fruit ahead of the deepest phase of Eliquis erosion.

As one of today’s largest cardiovascular brands approaching loss of exclusivity, Eliquis will be an important benchmark for how quickly revenues can decline once major markets transition to generics. The projected fall from around $14.bn in 2025 to well below $1bn within about five years illustrates the central theme of this analysis: heavy reliance on a single asset exposes large-cap pharma to rapid value erosion, making early diversification ahead of LOE events essential rather than optional.