Major growth in the anticoagulant market continued through 2017, primarily due to the increasing global prevalence of multiple cardiovascular (CV) indications including atrial fibrillation, acute coronary syndrome, peripheral artery disease and venous thromboembolism. However, cheap and established anticoagulants such as warfarin and heparin continue to present a barrier for new anticoagulant entrants.

After the launch of the novel oral anticoagulants (NOACs) almost a decade ago, encouraging NOAC clinical trial data along with increased experience managing patients taking NOACs, has led physicians to acknowledge that the drugs offer several benefits. Advantages include the fact that they do not require regular monitoring and are known to be safer and non-inferior – if not superior – in efficacy to the historical anticoagulants (warfarin and heparin). All of the aforementioned attributes have led to the enormous success of these agents.

Go deeper with GlobalData

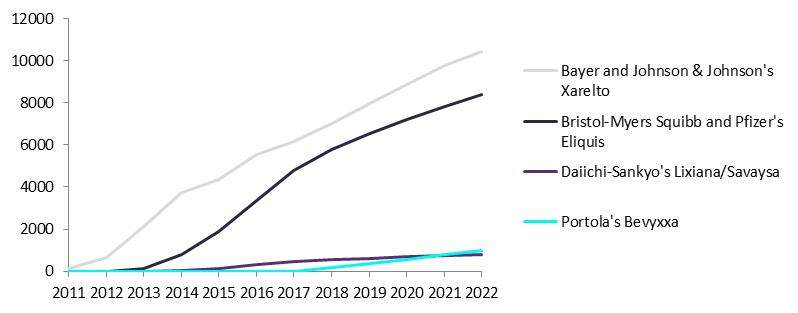

Despite the first marketed NOAC, Boehringer Ingelheim’s Pradaxa (dabigatran), soon facing generic erosion, the NOACs – specifically, direct factor Xa inhibitors (Xarelto [rivaroxaban], Eliquis [apixaban], Lixiana/Savaysa [edoxaban], and Bevyxxa [betrixaban]) – will dominate the CV market for years. Historical and projected sales for branded NOACs, specifically direct factor Xa inhibitors, can be seen in the figure below, with Bayer and Johnson & Johnson’s Xarelto and Bristol-Myers Squibb and Pfizer’s Eliquis leading in overall global sales.

Figure: historical and projected global sales of branded NOACs, direct factor Xa inhibitors ($m)

The ongoing arrival of anticoagulant reversal agents (for example, Boehringer Ingelheim’s Praxbind [idarucizumab] and upcoming Portola Pharmaceuticals’ AndexXa [andexanet alfa]) that could be employed in the case of a serious bleeding event, are poised to give NOAC developers an additional marketing boost.

In 2017, NOACs continue to dominate the anticoagulant landscape, but there are promising pipeline agents that are being developed. Ionis and Bayer are developing IONIS-FXIRX, a second-generation antisense anticoagulant drug in Phase II clinical trials that separates antithrombotic activity from bleeding risk. GlobalData expects IONIS-FXIRX to launch in 2022. There is also tecarfarin, a novel vitamin K antagonist in Phase III clinical trials for patients with prosthetic heart valves and renal insufficiency. GlobalData expects tecarfarin, being developed by Espero and Armetheon, to launch in 2023.

Related Reports

GlobalData (2017). PharmaPoint: Venous Thromboembolism – Global Drug Forecast and Market Analysis to 2026, June 2017, GDHC144PIDR

GlobalData (2016). PharmaPoint: Atrial Fibrillation – Global Drug Forecast and Market Analysis to 2025, August 2016, GDHC133PIDR

GlobalData (2016). PharmaPoint: Acute Coronary Syndrome – Global Drug Forecast and Market Analysis to 2025, August 2016, GDHC131PIDR