Type 2 diabetes (T2D) is a chronic disease characterised by insulin resistance and pancreatic β-cell failure, with an underlying genetic predisposition that is heavily influenced by diet and lifestyle. In 2016 alone, it was estimated that there were over 120 million diagnosed prevalent cases of T2D in nine major markets (US, France, Germany, Italy, Spain, UK, Japan, China and India).

Although the early-stage (Phase I and earlier) pipeline harbours many novel agents to address the disease, ‘me-too’ drugs continue to dominate the late-stage (Phase IIb and later) pipeline, with some exceptions such as Poxel’s imeglimin.

Go deeper with GlobalData

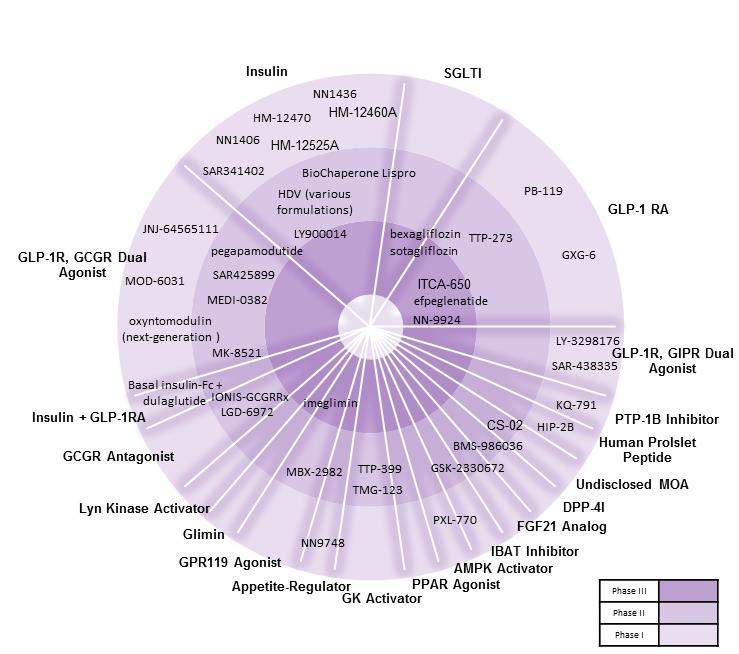

As seen in the figure below, the current late-stage T2D pipeline consists mostly of glucagon-like peptide-1 receptor agonists (GLP-1RAs) and sodium-glucose co-transporter inhibitors (SGLTIs), whereas the early-stage pipeline comprises a number of novel agents including G protein-coupled receptor 119 (GPR119) agonists, glucokinase (GK) activators, protein tyrosine phosphatase 1B inhibitors, and glucagon-like peptide 1 receptor (GLP-1R)/glucagon receptor (GCGR) dual agonists.

Figure: Type 2 diabetes agents in clinical development

Source: GlobalData, Pharma Intelligence Center [Accessed March 15, 2018]. ©GlobalData

After small molecules, peptides are the top molecule types for type 2 diabetes pipeline drugs in early-stage development. About half of the early-stage drugs are small molecules (49%), and a third are peptides (33%). Peptides are the most common molecule type for acting on GLP-1Rs and insulin receptors, which are the top targets for T2D pipeline agents. A total of 71% and 88% of early-stage GLP-1R and insulin receptor-targeting products are peptides, respectively. Monoclonal antibodies, which are the third most common therapy, work by preventing the breakdown of β-cells, resulting in higher insulin levels.

Despite the growing number of candidates in the T2D pipeline, key opinion leaders (KOLs) interviewed by GlobalData have repeatedly communicated that marketed and pipeline ‘me-too’ T2D drugs fall short of meeting one of the most pressing unmet needs in the space: sustained glycemic control, with a focus on decreasing insulin resistance and preserving β-cell function. As such, KOLs have largely shifted their sights from the ‘me-too’ populated late-stage pipeline to the early-stage pipeline in the hopes that novel treatments will help address the aforementioned unmet need.

Related reports

GlobalData (2018). Obesity: Competitive Landscape to 2026, to be published

GlobalData (2018). Type 1 Diabetes: Competitive Landscape to 2026, to be published

GlobalData (2018). Type 2 Diabetes: Competitive Landscape to 2026, March 2018, GDHC004CL

GlobalData (2017). PharmaPoint: Type 2 Diabetes – Global Drug Forecast and Market Analysis to 2026, July 2017, GDHC152PIDR

GlobalData (2016). OpportunityAnalyzer: Diabetic Foot Ulcers – Opportunity Analysis and Forecast to 2025, December 2016, GDHC064POA

GlobalData (2015). PharmaPoint: Type 1 Diabetes – Global Drug Forecast and Market Analysis to 2023, March 2015, GDHC105PIDR

For more insight and data, visit the GlobalData Report Store – Pharmaceutical Technology is part of GlobalData Plc.