Shortages of medicines for conditions such as diabetes, attention deficit hyperactivity disorder (ADHD) and hormone replacement therapy (HRT) have long been a feature of the healthcare landscape, but recent events have thrown the issue into starker relief.

Back in 2016, the World Health Organization acknowledged the scale of the problem was such that it affected nations of all sizes, and called for a global approach to address the essential medicine shortages being reported in high-, middle- and low-income countries.

Go deeper with GlobalData

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

In the decade before that publication the situation was already very concerning. New drug shortages in the US rocketed from 70 instances in 2006 to 267 in 2011. Meanwhile, a survey published in 2014 by the European Association of Hospital Pharmacists found 21% of hospital pharmacists experienced a shortage of medicines every day, and for 45% of those questioned this was a weekly problem.

Such stock absences prevent pharmacists from dispensing prescriptions and mean hospitals lack the supplies they need, all of which have a very real impact on patients, but it has proved to be a long-standing problem because it is such a difficult one to tackle.

Medicine shortages have multifactorial, interrelated causes. They can stem from underlying economic, business, political, manufacturing and distribution issues, or might be traced back to one or more flareups around a specific raw material shortage or a problem with manufacturing capacity at a particular facility.

Waves of pharma supply chain disruption

COVID-19 was a case study in how far supply chains could be stress-tested, as countries around the world went into lockdown, affecting the manufacturing, supply, and distribution of medicines. Increased demand for medicines used to treat patients with the virus, including anesthetics, antibiotics, and muscle relaxants, also contributed to greater shortages during the pandemic.

Since then, medicine supply has faced geopolitical shocks, with the ongoing conflict in Ukraine contributing to a general worsening of an already poor situation. In 2025, a report from the UK’s All Party Parliamentary Group on Pharmacy concluded that shortages had “shifted from isolated incidents to a chronic, structural challenge”.

The situation in Ukraine was also not the last geopolitical shock to the system. Now the world is grappling with how to respond to another era-defining event – the US and Israeli attacks on Iran and the subsequent closure of the vital trade route through the Straits of Hormuz. At the time of writing, it has been just over two months since the strikes on Iran, and the war shows no signs of ending.

As it stands, the Middle East conflict has exposed real vulnerabilities in supply chains. The first month of the conflict stalled 20% of the global oil supply and disrupted 18% of air cargo, with the latter an issue for the vaccines and biologics medicines that are typically transported by plane due to their specific storage conditions. But, as trade was disrupted and transport costs soared, concerns focused on the vital raw materials and active pharmaceutical ingredients (APIs) needed to make medicines and their cross-border production.

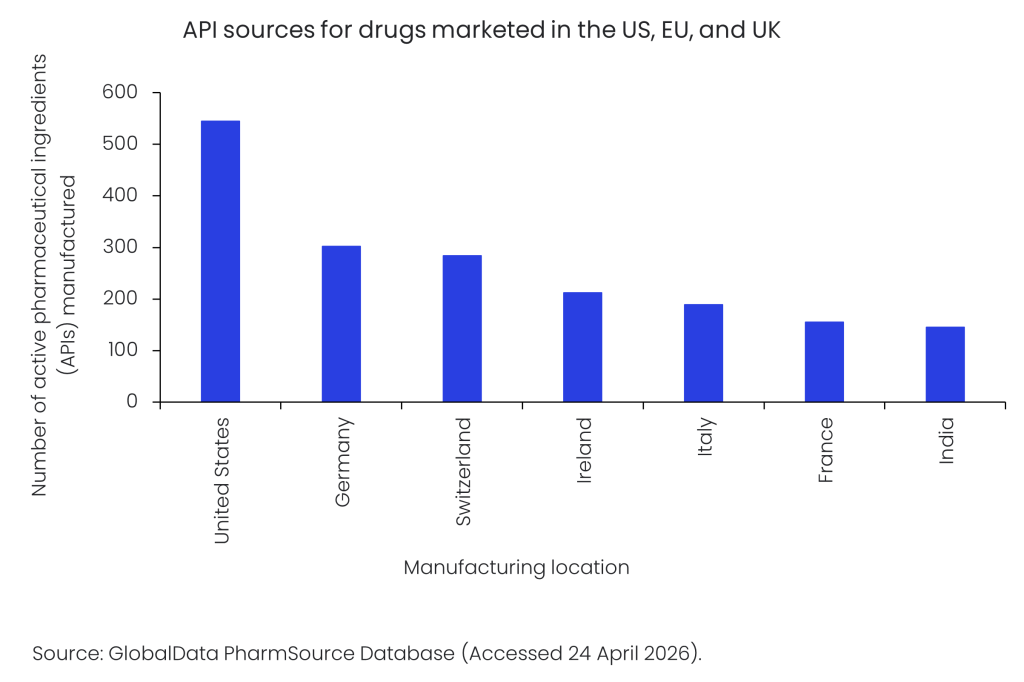

For the innovator and biosimilar therapies approved in the US, EU or UK, significant proportions of APIs are produced by European countries and India, even though the US is the single biggest manufacturer.

However, cross-border trade is an inherent part of API sourcing, and the US, EU and UK all import at least half of the APIs they need from other regions, with, for example, less than a third (32%) of APIs needed by the US coming from local North American suppliers, according to GlobalData’s PharmSource database.

Holding back the tide of medicine shortages

The global distribution of the pharma supply chain, which goes beyond where their APIs are sourced to encompass where drugs themselves are manufactured, poses clear risks to the availability of medicines.

Just as none of the developed markets of the US, EU and UK currently fulfills all their API needs from homegrown sources, a similar picture emerges for the manufacturing of innovator and biosimilar therapies approved for use in those countries. In the EU, for example, domestic manufacturers produce less than half (47%) of the innovator and biosimilar therapies approved in the region, according to GlobalData’s PharmSource database. Just over a third (37%) of the EU’s requirements have a transatlantic source, with their manufacturing taking place in North America.

Against this background of structural challenges, in which global sourcing has often struggled to meet demand, and repeated geopolitical shocks, countries are beginning to turn to stockpiling to ensure medicine supply resilience.

In the US, President Donald Trump issued an August 2025 executive order that called for the creation of an API stockpile to cover around 26 ‘critical drugs’, with Bristol Myers Squibb, GSK, and Merck among the pharma companies subsequently stepping forward to contribute to it. For its part, the EU is using the new Critical Medicines Act, finalised in January 2026, to build stockpiles, as it focuses on the issue of medicine security. However, the UK currently has no plans to create either stockpiles of medicines and APIs or the kinds of public lists that would help facilitate such a course.

Even where there are plans in place to build medicine and API stockpiles, it takes time to do so, they do not last forever, and it is not an appropriate approach for all types of medicines. Vaccines and injectable medicines in particular present immediate vulnerabilities due to their cold-chain storage requirements.

National security undercurrents

Countries are increasingly taking a ‘nation-first’ approach to their domestic supply chains as they respond to the long-standing production tensions, with the Middle East conflict creating an additional sense of urgency for the issue.

National responses are in some ways exemplified by Trump’s push to onshore pharma manufacturing. Although it is an agenda with predominantly economic goals, it will have second-line health security benefits as companies such as Eli Lilly, Johnson & Johnson and GSK expand their US manufacturing footprints. It also plays into political concern in the US about the rise of China and how its low-cost manufacturing base has “captured America’s drug supply”, as a recent Senate committee hearing termed it. The US imposition in April 2026 of up to 100% tariffs on pharma imports is an additional lever that is enthusiastically being pulled by Trump to further encourage onshoring.

In Europe, the EU’s Critical Medicines Act has, in addition to its stockpiling focus, aims of securing the region’s supply chains on a much wider basis by supporting the onshoring of API, critical medicine, and essential drug production. Meanwhile, the UK has yet to go that far, but the country has joined the EU’s Critical Medicines Alliance as an associate member to be part of the dialogue around the issue.

The future flow of medicines

The conflict in the Middle East presents the starkest warning yet of the entrenched global vulnerabilities to medicine supply chains. Even when a resolution is achieved between the US, Israel and Iran, the short- to medium-term shocks will take a long time to dissipate as the system reacts to higher costs for fuel and raw materials.

The war has turbocharged countries’ thinking around medicine security and the moves in that direction by the US and EU are expected to improve the situation for those geographies, but there is no quick fix for such a thorny problem. New factories take time to build and bring up to Good Manufacturing Practice (GMP) standards, and it will be difficult to redraw the globalised lines of pharma supply chains. Nevertheless, the direction of travel is clear, and the manufacturing of medicines will be quite different in the future.