Hiring in healthtech across North America has been contracting since mid-2025, and May 2026 data confirmed the trend has not broken. The aggregate number, however, conceals a picture that is far more differentiated: divided by company, by theme, and by the seniority of roles still being filled.

Active job postings in healthtech fell consistently from a June 2025 peak of 8,728 to 5,188 by May 2026, a decline of more than 40%, with year-on-year comparisons turning sharply negative from November onward. This is not seasonal noise.

The scale of the reversal is the context. Hiring in healthtech expanded aggressively through mid-2025, with year-on-year active posting growth running at 87 to 99% as recently as August and September 2025. The correction since then is structural. Companies are not merely posting fewer roles; they are also closing them faster, with closed postings running consistently above new postings in recent months. Critically, average job duration has held stable through the decline. Volume contracting while velocity holds is consistent with deliberate de-stocking of open roles, not a hiring freeze. The signal is directional, not distressed.

Top-decile names up 80%, bottom-decile down 60%

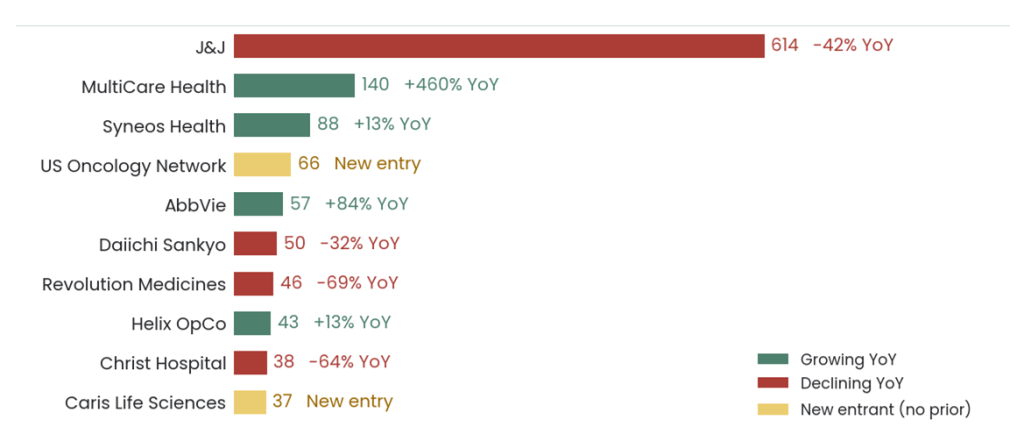

The cross-section of year-on-year hiring change in healthtech is unusually wide. Top-decile names are running at +80% or above; bottom-decile names are down 60% or more. That dispersion is the harvestable part; it is not visible in the aggregate number. Johnson & Johnson remains the volume leader at 614 postings in May but is down 42% year-on-year. The Christ Hospital is down 64% and Revolution Medicines has shed 69% of its posting volume over the same period.

Against that backdrop, AbbVie is ramping while J&J cuts. AbbVie posted 57 roles in May, up 84% year-on-year; Syneos Health grew 13%, which carries particular weight given that contract research organisations are typically the first to absorb any contraction in pharma discretionary spend. MultiCare Health System is up 460% from a low base. Two further names, The US Oncology Network and Caris Life Sciences, appear in May’s top ten with no prior-year comparable. In a contracting month, new entrants of that kind are not filling gaps; they are starting something. Counter-cyclical hiring at this scale is rarely accidental.

Senior share held through the contraction

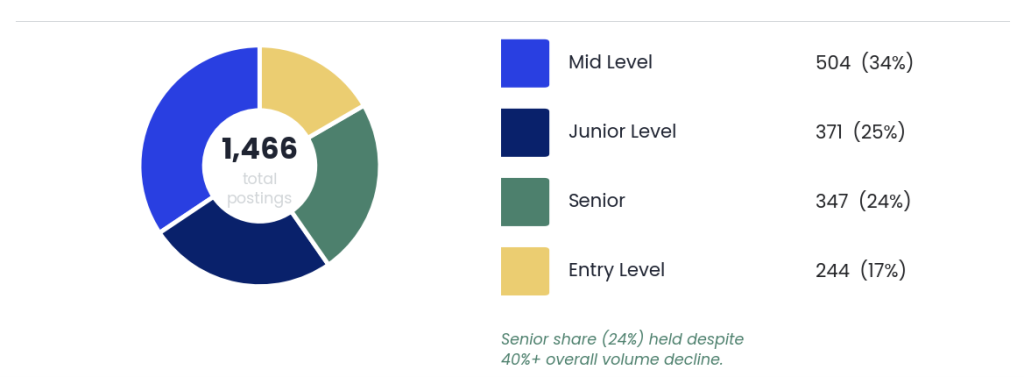

The instinct is to read mid and junior level as the dominant seniority bands and conclude that companies are sustaining operations rather than building. However, that reading is incomplete. Despite lower overall volume, senior hiring has held its proportional share, sitting close to junior postings and well above entry-level. With total volume down, every senior hire now represents a larger share of a smaller budget. The fact that senior concentration has held is not passive; it is a revealed preference. Companies under volume pressure are choosing depth over breadth.

Senior roles at a company like AbbVie, which is growing its posting volume counter-cyclically, carry a different signal than senior postings at a company cutting overall headcount. When volume falls but the senior ratio holds, the workforce is being reshaped, not reduced. The two dimensions read together – volume direction and seniority composition – produce a more precise picture of strategic intent than either does in isolation. A portfolio screen that combines both will rank companies differently than one built on volume alone.

Top three themes have two-to-four-year build cycles

Precision and Personalised Medicine lead all hiring themes, followed closely by Big Data, Supply Chain, and Artificial Intelligence, according to GlobalData Jobs Analytics. None of the top three are operational categories or short-cycle commitments. Build timelines in precision medicine, AI, and genomics run two to four years at minimum; companies hiring into them during a broad contraction are making a statement about where they expect to compete, not where they are managing costs. The thematic composition of what remains is skewed toward capability that takes years to unwind, which is precisely what makes it a durable signal.

Virtual Care and Genomics also feature among the leading themes, consistent with a market in selective investment mode rather than broad retreat. Supply Chain reads differently: its continued strength reflects an ongoing structural reconfiguration that predates the current contraction, as companies across the pharma value chain continue to address post-pandemic resilience gaps that have not yet closed. Those still hiring into these themes, against the broader decline, are the names worth tracking for forward strategic positioning.

Figure 4: Top Hiring Themes by Jobs Posted — Healthtech, North America, May 2026

The clean single-market factor

With well over 90% of postings in the US, the healthtech hiring signal in North America is effectively a single-market factor. That is a useful analytical property: geographic noise is low, the macro backdrop is homogeneous across names, and cross-company comparisons are not contaminated by country-level hiring conditions. All three geographies declined month-on-month in May 2026, with Canada and Mexico seeing somewhat steeper falls, but neither market is large enough to shift the factor.

At company level, J&J is the only name with a genuinely multi-market footprint across all three countries. Most peers are almost entirely US-concentrated, which reinforces the factor-purity point: the signal here is clean, with a homogeneous competitive and regulatory backdrop across the names in scope. J&J’s cross-border scale is the exception that confirms the rule.

The window closes fast

Hiring in healthtech is contracting, but the contraction is not uniformly distributed. The companies still investing, the themes still attracting postings, and the seniority profile of roles still being filled are where the forward-looking story lives. Aggregate volume is a lagging indicator; the composition of what remains is not.

Hiring intent moves faster than earnings calls, filings, or guidance. Job postings lead earnings revisions by one to three months on average; by the time the divergence between AbbVie and J&J surfaces in quarterly filings, the positioning window has largely closed. The interval between what companies are building and when it surfaces publicly is where the most consequential intelligence sits. A systematic read of that signal, across hundreds of millions of job listings, is what separates a data advantage from a data point. GlobalData Jobs Analytics delivers point‑in‑time postings direct from company career pages, tagged by company, sector and theme to set out the evidence directly: three indicators, seven years of data, and performance tested across every major market regime. Download the paper below or request a data sample by contacting hirendra.vikram@globaldata.com to start translating complex hiring patterns into straightforward signals you can use in planning and investment decisions.